Why audit third parties? Reduce risk and ensure compliance

- John C. Blackshire, Jr.

- Apr 26

- 10 min read

TL;DR:

Third-party relationships pose significant risks including data breaches, operational disruptions, and regulatory fines.

Effective audits are ongoing, risk-based cycles that verify controls rather than rely solely on contracts or questionnaires.

Implementing risk-tiered, continuous monitoring programs greatly enhances risk reduction and organizational resilience.

Third-party relationships are among the most consequential decisions an organization makes, yet they remain one of the least scrutinized. 59% of organizations suffered a data breach caused by a third party in the past year, with the average incident costing $4.45 million. Despite these figures, many compliance and risk teams still rely on signed contracts, basic questionnaires, or one-time due diligence reviews as their primary safeguard. That approach is no longer adequate. This article explains why rigorous third-party auditing is essential, how effective programs are structured, and what separates organizations that genuinely reduce risk from those simply performing compliance theater.

Table of Contents

Key Takeaways

Point | Details |

Third-party risk is substantial | A majority of data breaches and compliance fines stem from third-party vendors, demanding rigorous oversight. |

Continuous audits outperform annual checks | Ongoing, risk-tiered audits and automation reduce third-party risk exposure more than once-a-year reviews. |

Accountability culture beats checkbox compliance | Fostering ongoing accountability with vendors ensures real risk reduction instead of just ticking boxes. |

Effective audits require a modern strategy | Scalable, risk-focused audit frameworks and leadership engagement boost impact and ROI. |

The hidden risks of third-party relationships

To understand why auditing is vital, let’s examine the true scope and impact of third-party risk.

Third-party risk refers to the potential for harm arising from an organization’s reliance on external vendors, suppliers, service providers, or contractors. That harm can take several forms: data exposure, operational disruption, regulatory violations, financial loss, and reputational damage. What makes this risk category particularly difficult to manage is that the exposure often originates outside your direct control, inside systems and processes you cannot see without deliberate effort.

The empirical data is stark. According to third-party risk data, 74% of ransomware attacks are traced back through third parties, and 76% of GDPR fines are linked to third-party failures. These are not edge cases. They represent systemic vulnerabilities that exist across industries, from financial services to healthcare to manufacturing.

“The average third-party breach costs $4.45 million, and 59% of organizations experienced one in the past year alone.” This is not a theoretical risk. It is a recurring operational reality.

What makes the problem worse is the concept of “nth-party” risk. Your vendor has vendors. Those vendors have their own subcontractors. Each link in that chain represents an access point to your data and systems. A payroll processor, a cloud storage provider, a logistics partner, each one may connect to dozens of downstream suppliers you have never assessed. Basic due diligence at the point of contract signing does not account for this extended ecosystem.

The most common types of third-party risk include:

Data and cybersecurity risk: Unauthorized access, data leakage, or ransomware entering your environment through a vendor’s compromised systems

Operational risk: Vendor failures that disrupt your core business processes, such as a cloud outage or a logistics breakdown

Compliance and regulatory risk: A vendor’s non-compliance with GDPR, HIPAA, SOX, or other applicable regulations that exposes your organization to fines or enforcement actions

Financial risk: Vendor insolvency, fraud, or billing irregularities that create direct financial losses

Reputational risk: Public association with a vendor’s ethical violations, data mishandling, or legal problems

Contracts and service level agreements (SLAs) set expectations, but they do not verify performance. A vendor can sign every document you put in front of them and still operate with inadequate controls. The only way to know what is actually happening inside a vendor’s environment is to audit it.

How third-party audits work: Stages, standards, and best practices

With an understanding of risk, here’s how effective third-party audits are structured and what sets robust programs apart.

A structured third-party audit is not a single event. It is a repeating cycle of review, verification, and improvement. Per the standard audit cycle, a typical ISO 9001-aligned program moves through four distinct stages:

Stage 1 documentation review: The auditor examines the vendor’s policies, procedures, and documented controls before any on-site work begins. This stage identifies gaps in documentation and determines whether the vendor is ready for a deeper review.

Stage 2 on-site conformity audit: Auditors visit the vendor’s facilities or conduct a structured remote review to verify that documented controls are actually implemented and operating effectively.

Surveillance audits: Conducted annually between certification cycles, these shorter reviews confirm that controls remain effective and that no significant changes have introduced new risks.

Recertification audit: Performed every three years, this is a full reassessment that re-establishes the vendor’s conformance with applicable standards.

This cycle provides a framework, but the quality of what happens within each stage varies significantly between organizations. The table below illustrates the difference between compliance-only audits and continuous, risk-based audit models:

Dimension | Compliance-only audit | Continuous, risk-based audit |

Frequency | Annual or point-in-time | Ongoing with periodic deep reviews |

Scope | Fixed checklist | Prioritized by risk level |

Trigger | Calendar schedule | Risk events and threshold alerts |

Outcome focus | Documentation complete | Actual risk reduction |

Regulatory posture | Reactive | Proactive |

Cost efficiency | Lower upfront, higher breach cost | Higher upfront, lower breach cost |

Standards such as ISO 9001, SOC 2, and NIST SP 800-53 provide the technical benchmarks that give audits their authority. These frameworks define what “good” looks like across security controls, data handling, operational continuity, and quality management. Organizations that anchor their vendor audits to recognized standards are better positioned to defend their oversight programs to regulators and boards.

Pro Tip: Integrating automated continuous monitoring tools into your vendor oversight program can reduce third-party risk exposure by up to 40%. Tools that track vendor security ratings, certificate expirations, and public breach disclosures in real time allow your team to act on emerging issues rather than discovering them at the next scheduled review. Learn how continuous auditing methods can deliver measurable compliance ROI.

Best-in-class programs blend manual judgment with automation. Automated tools flag anomalies and surface data at scale. Human reviewers then apply professional judgment to determine whether a flagged issue represents a genuine control failure or an acceptable deviation. Neither element alone is sufficient.

From checkbox compliance to continuous accountability

Understanding the stages is critical, but how you approach auditing shapes outcomes. Let’s dig into the difference between basic compliance and true accountability.

The checkbox audit mentality is seductive because it feels like progress. A questionnaire goes out, responses come back, a score is calculated, and the vendor passes. The file is closed for another year. Everyone moves on. The problem is that this process measures a vendor’s ability to answer questions correctly, not their actual control environment.

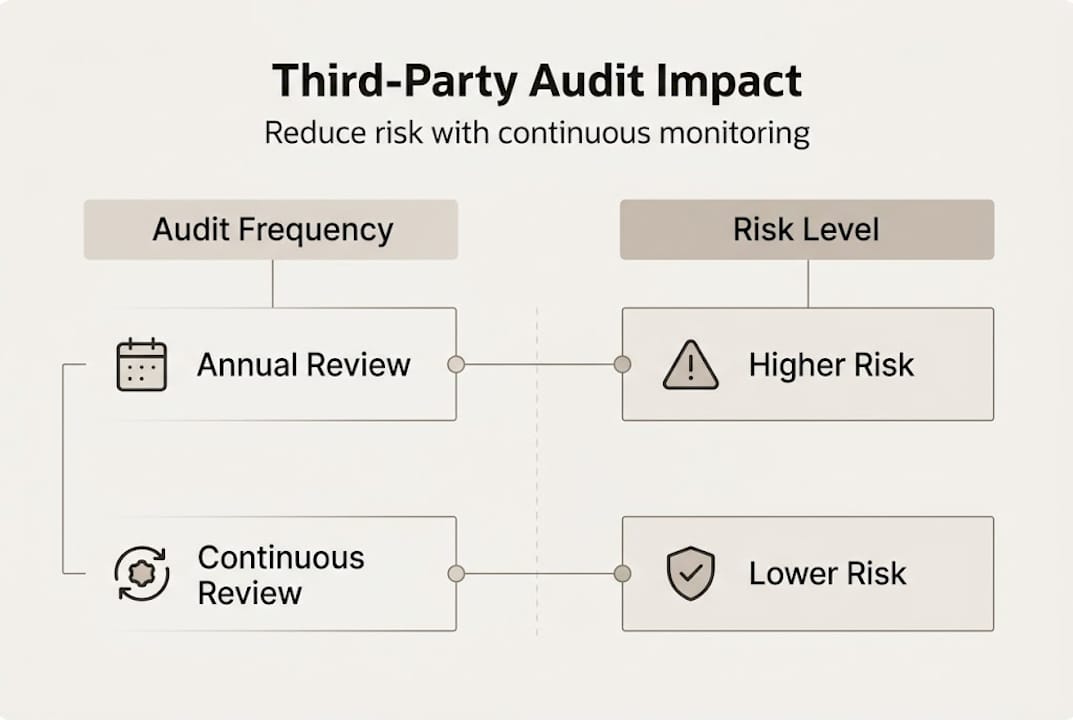

Continuous monitoring reduces risks by 40% compared to periodic, compliance-focused reviews. That gap exists because risk does not pause between audits. A vendor that passed your annual assessment in January may have experienced a significant personnel change, a system migration, or a subcontractor relationship in March that fundamentally altered their risk profile.

The following table contrasts the measurable outcomes of each approach:

Outcome area | Checkbox compliance | Continuous accountability |

Risk detection speed | Months to years | Days to weeks |

Regulatory fine exposure | High | Significantly reduced |

Vendor relationship quality | Transactional | Collaborative |

Organizational resilience | Fragile | Adaptive |

Audit resource efficiency | Low (broad, unfocused) | High (risk-tiered) |

Building a culture of ongoing accountability requires more than technology. It requires organizational commitment across several dimensions:

Risk-tiered audit schedules: Not every vendor warrants the same level of scrutiny. Tier your vendors by criticality and data access, then calibrate audit frequency and depth accordingly.

Vendor engagement beyond the audit: Share findings constructively. Treat vendors as partners in risk reduction, not adversaries to be caught. Vendors that understand your expectations and see value in the relationship are more likely to maintain strong controls.

Cross-functional involvement: Third-party risk is not solely a compliance function. Procurement, IT, legal, and operations all have visibility into vendor relationships that a compliance team alone cannot replicate.

Defined escalation paths: When a vendor fails to remediate a finding within an agreed timeframe, your program needs a clear, pre-approved escalation process, up to and including contract termination.

Pro Tip: When communicating audit expectations to vendors, frame requirements in terms of mutual benefit. Vendors that understand how strong controls protect their own reputation and business continuity are more likely to engage seriously with your program. Pair this with audit ethics in practice to ensure your team models the accountability standards you expect from vendors.

The shift from continuous auditing as a concept to continuous auditing as a practice is where most organizations stall. The tools exist. The frameworks exist. What is often missing is the internal will to move past the comfort of a completed checklist.

Optimizing third-party audits for real impact

Moving past the basics, here’s how to build an audit program that truly reduces risk and protects your organization.

Effectiveness in third-party auditing is not about volume. Auditing every vendor with the same intensity is neither practical nor efficient. The goal is to concentrate your most rigorous oversight on the relationships that pose the greatest risk to your organization. Here is a structured approach to building a scalable, risk-tiered audit framework:

Build a complete vendor inventory: You cannot audit what you have not cataloged. Start with a full inventory of all third-party relationships, including software, services, and data processors, regardless of contract size.

Tier vendors by inherent risk: Assess each vendor based on data sensitivity, operational criticality, regulatory scope, and geographic exposure. Assign each vendor to a risk tier that determines audit frequency, depth, and required evidence.

Define audit scope by tier: High-risk vendors receive full on-site or remote audits with evidence testing. Medium-risk vendors may receive structured questionnaires supplemented by automated monitoring. Low-risk vendors may require only periodic self-attestations with spot-check verification.

Integrate continuous monitoring: Deploy tools that track real-time signals, such as security ratings, breach disclosures, and financial health indicators, across your vendor population. Use these signals to trigger out-of-cycle reviews when warranted.

Close the loop on findings: Every audit finding must have an owner, a remediation deadline, and a verification step. An audit that identifies a gap but never confirms it was fixed has accomplished nothing.

Report to leadership regularly: Summarize third-party risk posture, open findings, and trend data for executive and board audiences at least quarterly. Leadership visibility drives resource allocation and organizational accountability.

Common pitfalls that undermine even well-designed programs include:

Internal silos: When procurement signs a vendor without notifying IT or compliance, risk assessments are incomplete from day one.

Ignoring nth-party risk: Auditing your direct vendors without understanding their key subcontractors leaves significant blind spots. High empirical breach rates confirm that attackers exploit these gaps deliberately.

Over-reliance on automation: Automated tools are powerful, but they cannot replace the professional judgment required to interpret findings in context. Refer to EMS operational audit insights for examples of how operational audits balance automation with human review.

Treating audit as a one-time event: Risk is dynamic. A vendor’s control environment changes constantly. Annual audits alone cannot keep pace.

Pro Tip: To secure leadership buy-in for continuous improvement, translate audit findings into financial terms. Quantify the potential cost of a breach from each high-risk vendor, then compare that figure to the cost of enhanced oversight. The return on investment becomes difficult to argue against when the numbers are on the table.

Connecting your audit program to recognized standards, such as those covered in external audit process training, also strengthens your regulatory defense posture. Regulators look favorably on organizations that can demonstrate a documented, risk-based, and consistently applied vendor oversight program.

Why most third-party audit strategies fall short—and what actually works

With these strategies outlined, here’s an unvarnished look at what often goes wrong—and what sets standout programs apart.

Most third-party audit programs are designed to satisfy auditors, not to reduce risk. That distinction matters more than most organizations acknowledge. I have seen programs where vendors pass annual reviews with near-perfect scores, only for a breach to occur six months later because the daily operational practices never matched the documented controls. The audit captured a snapshot. Reality kept moving.

The uncomfortable truth is that many organizations are performing compliance theater. The questionnaires go out, the responses come back, the scores look acceptable, and the program is considered healthy. But risk-tiered, continuous methodologies consistently outperform annual checks precisely because they reflect how risk actually behaves, not how it looks on a given review date.

What separates standout programs is not the sophistication of their tools. It is the organizational commitment to treating vendor oversight as an ongoing operational discipline rather than a periodic administrative task. That means cross-functional teams, executive sponsorship, and a willingness to act on findings even when it disrupts a valued vendor relationship.

The challenge I put to every compliance and risk professional reading this: audit your audit program. Ask whether your current approach would have detected the last major third-party breach in your industry before it happened. If the honest answer is no, the continuous audit ROI case for upgrading your methodology is already made.

Advance your audit expertise with practical training

For those inspired to strengthen their audit capabilities, here are training resources to accelerate your impact.

Effective third-party auditing requires more than process knowledge. It demands professional judgment, current regulatory awareness, and the practical skills to design and execute risk-based programs. At compliance-seminars.com, we offer NASBA-recognized CPE courses, live webinars, and in-person seminars delivered by practitioners with Big 4 backgrounds. Whether you are building your organization’s vendor oversight framework or preparing for a regulatory examination, our internal audit training and risk management courses give you the tools to move from compliance theater to genuine risk reduction.

Frequently asked questions

What is a third-party audit and why is it important?

A third-party audit is an independent review of a vendor’s controls and practices to verify compliance and identify risks before they affect your organization. Per the standard audit cycle, it typically includes documentation review, on-site conformity testing, and ongoing surveillance.

How often should third-party audits be conducted?

Annual surveillance audits are the standard minimum, with full recertification every three years, but continuous monitoring between formal audits provides significantly better risk control.

What are the main risks of not auditing third parties?

Organizations that skip structured vendor audits face substantially higher exposure to data breaches, ransomware, and regulatory fines. 74% of ransomware attacks are traced through third parties, and 76% of GDPR fines are linked to third-party failures.

How can we make audits more effective without being overly burdensome?

A risk-tiered approach concentrates your most intensive oversight on the highest-risk vendors while using automated monitoring and periodic self-attestations for lower-risk relationships. Risk-tiered, continuous methodologies deliver better outcomes without proportionally increasing audit workload.

Recommended

Comments